RealtyTrac® recently released a report analyzing purchase loan and sales data for single family homes and condos in 2014 in 386 counties nationwide which found that on average across all counties, buyers who purchased a home in 2014 put 14 percent down, translating into an average $32,141. Nearly 1.5 million purchase loans were included in the analysis.

RealtyTrac® recently released a report analyzing purchase loan and sales data for single family homes and condos in 2014 in 386 counties nationwide which found that on average across all counties, buyers who purchased a home in 2014 put 14 percent down, translating into an average $32,141. Nearly 1.5 million purchase loans were included in the analysis.

“This analysis shows that first time homebuyers have a better shot at buying a home in low-priced markets, not just because of the lower price point but because on average buyers are putting down just 12 percent in those markets compared to 24 percent in high-priced markets,” says Daren Blomquist, vice president at RealtyTrac. “Meanwhile, the markets where millennials are moving the most have above-average down payment percentages, which will make it tough for millennial renters to convert into first-time homebuyers in those markets.

“There are a few exceptions, however, where the combination of an influx of millennials and relatively low average down payment percentages indicate markets that will see a quicker return of the first-time homebuyer,” Blomquist added. “Markets such as Nashville, Durham, Philadelphia, Des Moines, Little Rock and Columbus, Ohio.”

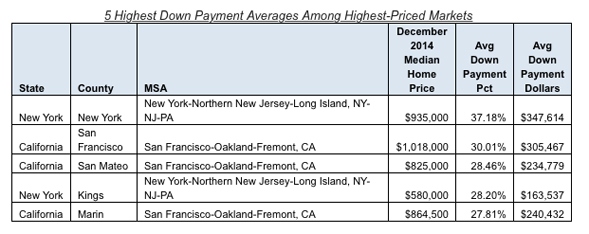

Down payments average 24 percent in highest-priced markets

In the 25 counties with the highest median home sales prices at the end of 2014, the average down payment percentage was 24 percent for homes purchased in 2014. The average down payment in dollars in these 25 counties was $138,547. On average, low down payment loans accounted for 7 percent of all home purchases in these counties in 2014.

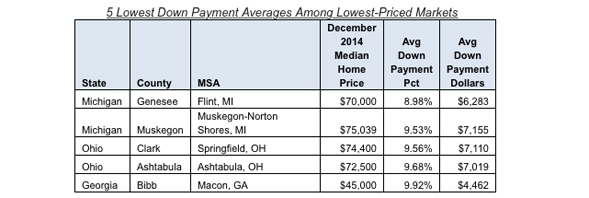

Down payments average 12 percent in lowest-priced markets

In the 25 counties with the lowest median home sales prices at the end of 2014, the average down payment percentage was 12 percent for homes purchased in 2014. The average down payment in dollars in these 25 counties was $8,239. On average, low down payment loans accounted for 25 percent of all home purchases in these counties in 2014.

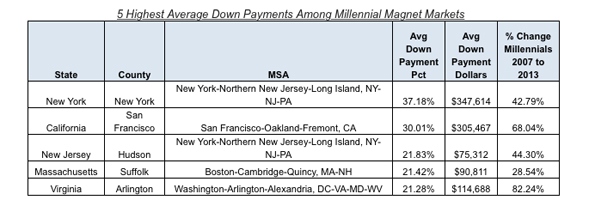

Average down payment 17 percent where millennials are moving most

In the 25 counties with the biggest increase in the millennial population between 2007 and 2013, the average down payment percentage was 17 percent for homes purchased in 2014 (above the national average of 14 percent). The average down payment in dollars in these 25 counties was $66,174 — more than twice the national average of $31,723. The average down payment percentage in these 25 counties was 17 percent (above the national average of 14 percent), and on average low down payment loans accounted for 15 percent of all home purchases in 2014 (compared to 18 percent on average among all counties analyzed).

Top 10 markets for first time homebuyers

RealtyTrac identified the top 10 markets for first time homebuyers based on the average down payment percentage being below the national average of 14 percent and an increase in the millennial population of 20 percent or more following the Great Recession.

“We are anticipating further growth of consumers taking advantage of low down payment options for purchasing homes across Ohio in 2015,” says Michael Mahon, executive vice president at an Ohio-based real estate company. “As greater equity continues to stabilize property values, lenders’ use of down payment assistance programs, FHA, Fannie Mae, Freddie Mac, and USDA rural housing loans will continue to grow in popularity with first time home buyers, as well as boomerang home buyers returning to an appreciating housing market.”

“After the great recession, the public is becoming more aware of the available lending opportunities in the market today. The pendulum has swung back to a strong lending environment. As the millennials continue to move into the market and the investors diminish we will see the number of low down payment loans increase,” says Mike Pappas, CEO and president of a real estate firm covering the South Florida market. “Home affordability is still near an all-time high in our market—which makes it still a great buying opportunity.”

“It’s clear that low down payment loans are being used by first-time and other entry level buyers in lower priced markets; however, even in higher cost markets, there are a wealth of homeownership programs available that could lower buyers’ down payment and closing costs,” says Rob Chrane, president and CEO of Down Payment Resource. “Programs in high cost markets may offer even greater down payment help, and income and home price limits are typically increased to fit the market. There’s a general lack of awareness among first time homebuyers about down payment programs which may be keeping more of them on the sidelines longer than necessary.”

For more information, visit www.realtytrac.com.

{kind=link}