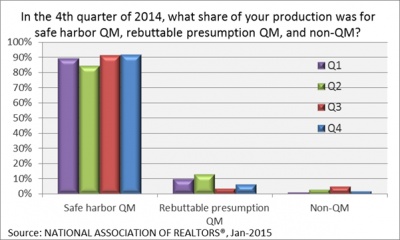

Fourth Quarter Highlights from the Lenders' LandscapeBy Ken Fears, Director, Regional Economics and Housing Finance NATIONAL ASSOCIATION OF REALTORS® Every quarter, NAR Research surveys a panel of mortgage originators about their recent lending activity as well as plans for the current period and beyond. In the 4th quarter of 2014, lenders’ confidence in non-Prime and non-ATR (ability-to-repay)/QM (qualified mortgage) products regained footing after pulling back in the 3rd quarter, but the mood remains pensive, looking for investor takeout. Lenders are optimistic about the future though, with recent policy changes having an impact, though legal actions by the government remain a concern. Market Dynamics After expanding to 5 percent in the 3rd quarter, the non-QM share of originations shrank to 1.8 percent in the 4th quarter. However, the rebuttable presumption share rose from 3.5 percent to 6.3 percent and the safe harbor segment of the QM market remained relatively constant at 91.9 percent.

Forty-five percent of respondents indicated having had an issue closing a loan in the 4th quarter due to some facet of the QM rule, down from 64 percent in the prior quarter. To prevent incursions of the QM rule, originators use buffers in advance of the 3 percent cap on points and fees, the 43 percent DTI (debt-to-income), and the pricing difference between near prime and subprime. After increasing in the 3rd quarter, the share of lenders using buffers eased. Furthermore, respondents’ confidence in their preparations for the QM/ATR rules leapt to 70 percent from 59.9 percent in the 3rd quarter. A year after the ATR/QM rule went into effect, half of respondents indicated that it had had a “small negative impact” on the market, while 35 percent cited a significant negative impact. Ten percent indicated no impact, while 5 percent reported a small improvement. The share of lenders offering rebuttable presumption and non-QM products was roughly unchanged from the 3rd quarter. However, willingness to originate non-QM mortgages flattened or fell only modestly from the 3rd to the 4th quarter after falling sharply over the prior two quarters. Lenders’ willingness to originate prime mortgages continued to gain steam even for those with lower credit scores. Respondents were more optimistic about the next 6 months expecting improvements in access for prime and near prime borrowers, but a more modest improvement for non-QM and little change for rebuttable presumption. Likewise, the majority expects improvement in investor demand across the board, but emphasized the prime segment. The Policy Front Seventy-five percent of respondents indicated that the GSE’s (government-sponsored enterprise) new 3-percent down payment product would improve access to credit, while 90 percent believed the Federal Housing Administration’s fee reduction will improve production with a weighted average increase of 8.5 percent. Eighty-five percent of respondents either had already or expected to expend considerable time preparing new forms and systems needed to comply with the altered RESPA/TILA (Real Estate Settlement Procedures Act/Truth in Lending Act) rules. Sixty-five percent felt that Consumer Finance Protection Bureau’s guidance had been at least adequate. Former homeowners who short-sold or were foreclosed on have begun to return to the market. Half of respondents indicated an increase in formerly distressed sellers seeking credit. Repurchase requests remain a concern, though, as 85 percent had been the subject of a GSE repurchase request. This factor was lenders’ primary concern about lending in the higher risk space. Only 40 percent indicated that recent overtures by the GSEs to clarify and soften representation and warranty risk would improve their willingness to originate higher risk mortgages, while 20 percent would wait-and-see. More clearly defined triggers for repurchase risk was the factor respondents felt would help most to improve credit access Finally, low housing supply, more than tight credit access or weak demand factors, was the leading factor holding back production according to survey respondents. While current conditions remain limited, in the 4th quarter originators were more optimistic about the future in part due to recent policy changes. However, concerns over government repurchase requests and weak investor takeout for non-QM products continue to be a headwind.

|

|

Ken Fears is Director, Regional Economics and Housing Finance, for the National Association of REALTORS®. For more information, visit

Ken Fears is Director, Regional Economics and Housing Finance, for the National Association of REALTORS®. For more information, visit

Brought to you by  © Copyright 2024, All Rights Reserved.

© Copyright 2024, All Rights Reserved.

© Copyright 2024, All Rights Reserved.